Business

FX & Bond View: The Return of MAGA

Published

7 months agoon

By

goaplusnews

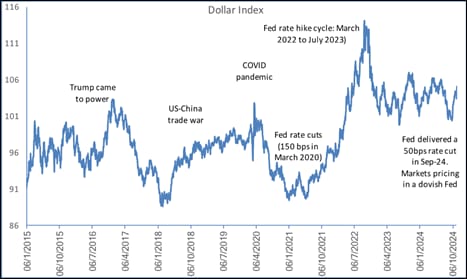

With Mr Donald Trump is set to become the next US president, the reaction across financial assets has varied. The expectation of deregulation and lower corporate taxes pushed the US stock market to an all-time high yesterday, while moves in the currency market were a different story. The US dollar index rose, recording its best day since 2020 while EM FX crosses came under pressure particularly the CNH and MXN – with China & Mexico expected to be hit the most with Trump’s policies. Moreover, DM currencies like the EUR, GBP, JPY also sold off against the US dollar. The USD/INR pair touched a new record low of 84.28, despite suspected RBI intervention that stalled its decline. In the bond market, US yields jumped up, with the 10-year rising by 15bps on rising fiscal concerns and expectations of a slowdown in the pace of future Fed rate cuts.

This reaction is part of the “Trump Trade”. In other words, the market is essentially gearing up for tariff increases (Trump has suggested 60% tariffs on Chinese imports and possibility of 20% on all US imports), further tax cuts and the fall out of these measures on US inflation, Fed policy action and US debt. We recognise that given the unpredictability of Mr Trump’s actions; one cannot presume that the past is likely to act as an exact blueprint of what’s to come. However, it does offer us with some clues. Based on this and Trump’s election promises, the existing inter-linkages between asset classes, and other macro and policy events due, we are laying out some bets for 2025.

Let’s start with growth. In the near-term, a Trump administration could lift US growth due to (likely) tax cuts and greater deregulation. But the medium-term implications are less straightforward. This is as tariffs hikes could be inflationary, negatively affecting consumer demand and hit US manufacturers dependent on global imports. Moreover, in the event of broader tariffs on all US imports – raising the risk of retaliation from other countries — global growth could slow down with economies like China and the Eurozone being especially vulnerable.

The Trump Trade: Although some pull back from the current exaggerated moves in financial markets are likely over the coming weeks, this so called “Trump Trade” is here to stay over the coming months. The US dollar is likely to retain ground against both EM and DM currencies. We see the US dollar index remaining bid well into the middle of 2025.

Moreover, elevated US yields and the rise in yield differentials with the Eurozone and UK, imply a weaker outlook for the EUR & GBP. We are switching our earlier neutral to slight bullish call on the euro with now expecting a further down move – with a possibility of the EUR/USD pair gravitating towards a range of 1.06-1.08.

For the US bond market, Trump 2.0 is likely to keep US yields elevated across the curve in the near-term. The long end of the curve could feel an upward pressure from fiscal concerns and an expected increase in bond supply. At the short end the increase could be slightly less as the market remains undecided on whether any future inflation risks could slow down the pace of Fed’s rate cuts. Therefore, we bet on the US yield curve steepening. For now, the Fed could continue its gradual path of rate cuts, and our base expectation is for a 25bps rate cut in both November and December, followed by 100bps rate cuts in 2025. To remind you, based on Trump’s recent comments, he is also likely to favour lower interest rates in the economy.

The China short: Rising threat of higher tariffs on Chinese imports, by the US, could put pressure on the already slowing Chinese economy, capital flows into Chinese assets and the Yuan in the near-term. This could possibly force China’s hand to respond by increasing stimulus measures (perhaps in the very near term) to lift sentiments. While this could help stabilise markets and the Yuan in the interim, we do not see these being enough to turn the tide in favour of China.

The Rupee and Domestic bonds: We recommend moving towards a more actively managed hedging strategy for the rupee. The USD/INR pair is likely to enter a period of somewhat increased volatility with the risk of larger moves over the coming months. Covering near-term risks (for the next 3-6 months) would be prudent.

We expect the rupee to depreciate further towards a range of 84.20-84.50 over the next 2-3 months, before moving to 84.50-85.0 in the first half of 2025. We do not rule out an eventual breach of the 85.0 level over the next 8-12 months for the pair. A rise in the US dollar, weaker Yuan and EM peers, and rising US yields are likely to exert pressure on the pair. However, we do believe that lower oil prices coupled with rotation of capital away from China to India could offer some support. The RBI is likely to continue active intervention in the FX market to stall the depreciation pressure on the rupee and prevent any panic run offs. That said, it would likely refrain from fighting against the wind and strongly defending any specific levels for the pair. Moreover, given overvaluation concerns and to keep the rupee competitive – especially with a weakening Yuan – the central bank could prefer an orderly depreciation in the rupee over the coming year.

For domestic yields, we see the 10-year bond yield trade in a range of 6.80-6.90% in the near-term on the back of pressure from higher US yields, volatile foreign bond flows and with the RBI refraining from moving towards rate cuts anytime soon. Given the lingering risks on inflation and possibility of inflation coming in higher than RBI’s projections (we expect CPI inflation to print at 6.1% in October) could keep the central banks’ guard up for longer. For Q4 FY25, we see the 10-year bond yield moving to a range of 6.75-6.80% on the back of more favourable supply and demand conditions in the domestic market (markets could price in the likelihood of lower bond supply than the initial BE target).

Beyond the Trump Trade: Some considerations

Looking beyond the Trump trade, once the market works out through the various implications of higher US inflation, pressures on debt and impact of tariffs on growth, we could see a counter narrative set it which is likely to lower both the US dollar and yields. Moreover, an attempt to talk down the US dollar by the Trump administration – given Trump’s comments on preferring a weaker dollar – could temper the rise in the US dollar over the medium-term.

The potential for a full-blown US-China trade war also looms large, with China likely to explore retaliatory measures including export restrictions (on agricultural products, critical minerals etc.) and tariffs, selling US treasuries, devaluing the yuan and further reorienting trade linkages with countries in LATAM and Europe instead.

Such a scenario could have mixed implications for Asian emerging markets over the medium-term. On the one hand, it could further push the move towards the China + 1 strategy, benefiting exports from countries like India. Moreover, India could benefit from further rotation of capital from China to India. On the other hand, higher US tariffs on Chinese imports could also add to the already rising domestic overcapacity in the country and increase the threat of this oversupply finding its way into other markets like India, hurting domestic manufacturing.

Implications for India of a Trump administration could also include renewed H1B visa restrictions, impacting Indian IT professionals working in the US.

Geopolitics: A Trump administration could likely amplify support for Israel, potentially encouraging a quicker resolution in the Middle East. His stance may also increase the likelihood of brokering an end to the Russia-Ukraine conflict, potentially easing pressure on global oil and natural gas prices.

Commodities: Trump’s policies on fossil fuels are likely to be supportive — expected to cut regulations and support an increase in oil production. We continue to therefore see oil prices trending lower and averaging close to $70 pbl in 2025.